El Salvador and Bitcoin: Perfect Bedfellows?

Could it really tick so many boxes, or are we missing something?

I couldn’t go to Miami’s Bitcoin Conference this year because post-COVID-19 travel restrictions from the U.K. meant it was just way too complicated.

Like thousands of others, I had to settle with the livestreams instead which, if truth be told, didn’t succeed in reducing my desire to be there.

In fact, it had the opposite effect.

On the Saturday, having been given a heads up by various heavyweight Bitcoiners that “something big” was coming, my other half and I watched Zap founder Jack Mallers’ emotional speech live as it unfolded.

The tears from Jack were entirely genuine, and we found ourselves in the same state. For years, I have been writing about how Bitcoin can change the world for people who have almost no chance otherwise of getting out of their situation. Suddenly — very suddenly, in fact — it was happening.

It’s something I genuinely believe the world needs to be able to start the next stage of human development. It’s also something I intend to do more of personally in the future. The bottom line was that thanks to Mallers’ admirable efforts in the country in the preceding months, El Salvador had announced that they were adopting Bitcoin as a national currency.

Within just four days, the bill was presented — and passed — in government. It’s official. By around Sept. 8, 2021, merchants will be required to accept bitcoin for all goods and services throughout the country. Just hours later, Wikipedia and Google Maps were updated to reflect the change.

Of course, those of us who have been in the Bitcoin space for some time knew this day was coming. We also knew that the first mover was most likely to be either a pariah state giving two fingers to the dollar, a hyperinflating economy trying to save themselves from ruin or a simple emerging economy that was forward looking enough to take the chance. El Salvador slips, mostly, into the latter category.

But I’ll be honest. I didn't have it on my short list. In retrospect, however, it now seems like an obvious, if not perfect choice.

So, what does the law say, and what does it really mean for the citizens of El Salvador and the future of Bitcoin?

A Simple Law

In countries like the U.S. and the U.K., we’re used to laws taking months or even years to pass, and then, when they do eventually go into effect, consisting of extremely complex telephone-directory length documents requiring numerous iterations to get exactly right.

President Nayib Bukele’s law was just three A4 pages written in plain language and passed with 64 votes out of a possible 82, more than enough to do the job, and it was greeted with great applause in the official chambers. The whole process took some four days.

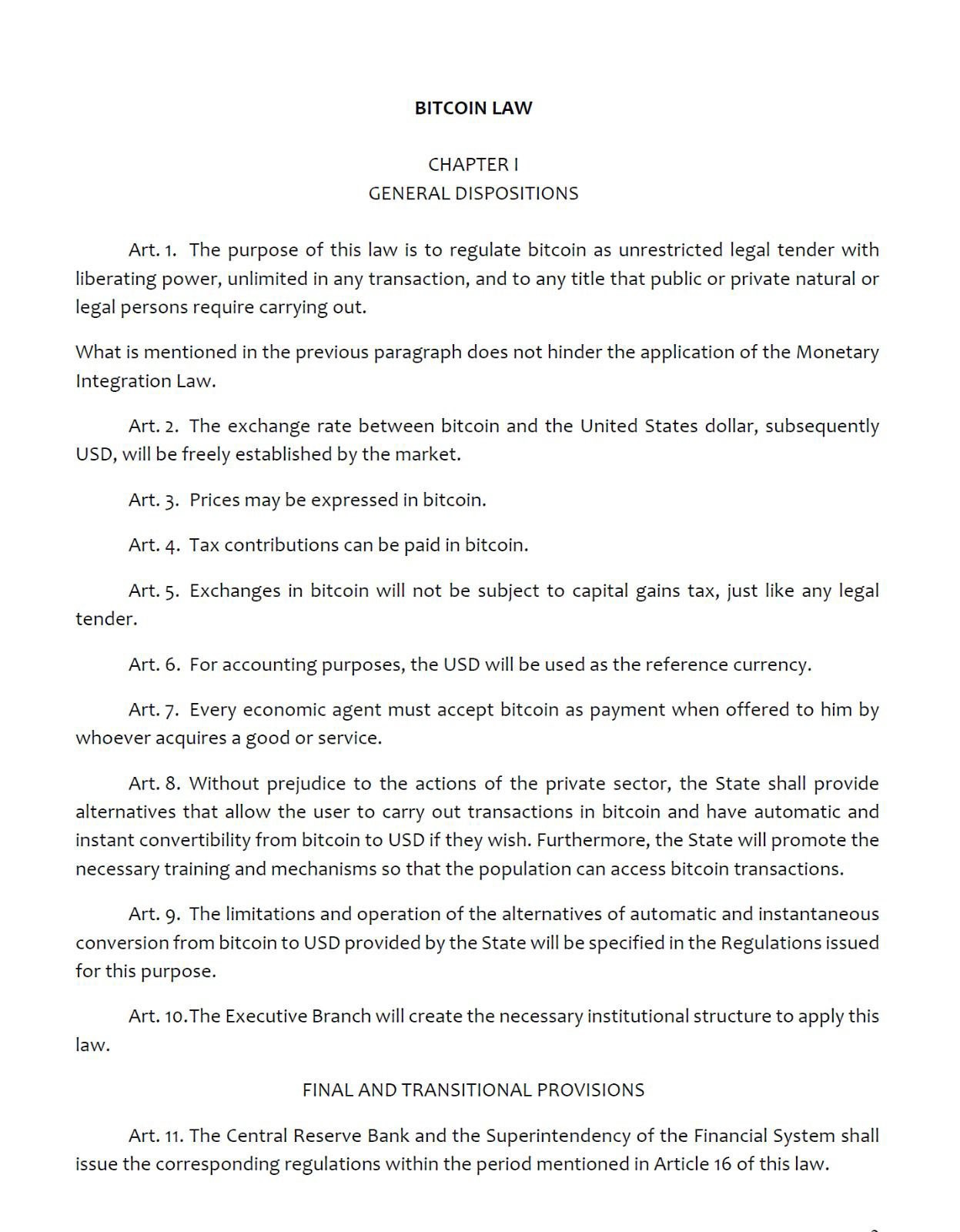

The law, as simple as it is, makes fascinating reading and contains several key statements. The above image shows the second page which contains the most important elements of the law.

First, that prices may be expressed in bitcoin. Of course, this may not be so straightforward to implement, given the fluctuations in both the price of bitcoin and the U.S. exchange rate. This will take some getting used to in the short-term both in terms of interpreting and presenting.

El Salvador had no national currency of its own, having switched to U.S. dollars for trade both within the borders and outside them in 2001 from the sovereign colon that preceded it. Interestingly, I understand that colones are also still (technically) legal tender, though not used in practice.

Second, it’s important to note that taxes can also be paid in bitcoin. This effectively reinforces the state’s assertion that bitcoin is truly a national currency.

Next, since bitcoin is treated as a currency within the border, it can’t be liable for the capital gains tax that other countries have imposed where, generally speaking, it is treated as an asset with taxable gains. Again, whilst an obvious point in many ways, it remains another state-level endorsement.

That said, Article 6 explains that accounting for these transactions will remain in the U.S. dollar, though it is not yet clear what approach will be taken here. This makes sense for what may well turn out to be a transitional period of moving between currencies. Should Bitcoin's state-level adoption continue throughout the world, there may well come a time when this article is no longer needed.

That’s quite a thought.

The last few sections shed some light on what this means “on the ground.” Essentially, all merchants for all goods and services are obliged to accept bitcoin at point of sale, if that is indeed what the customer wishes to pay with by the time the law comes into place.

They are also able to opt out if they don't demonstrably have the facilities to manage it and they can convert it straight to the U.S. dollar if they wish using a government scheme designed for that purchase.

It seems they have thought of everything — and in just a few hundred words.

It’s impressive, but the more you look into this, the wider-ranging the implications become.

The law in practice

My first reaction was concern over people being able to physically accept bitcoin even where the law clearly — and specifically — allows for that.

However, I then discovered through myriad sources that bitcoin acceptance is close to ubiquitous anyway in some parts of the country. In short, much of the infrastructure and understanding is already there, thanks to ongoing work over the last few years by passionate groups of people looking to rebalance the 70% of the population who have no access to banking facilities at all. (Source: Jack Mallers) In fact, in some cases, it is actually the preferred method of payment.

And where there isn’t yet the infrastructure in place, it appears there is sufficient momentum to make it happen.

But there’s a bigger element to this. Since all businesses are now obliged to accept bitcoin by early September, it means that even large, foreign business who have traditionally have had no incentive to experiment with it must now do so. Yes, that includes McDonald's, car dealerships (even Tesla!), Apple stores and just about anything you can think of.

This means that Bitcoin acceptance is not only happening at state level, it’s also happening at a commercial level. If a company such as McDonald’s can do it in El Salvador (it will be difficult for these companies to show they can’t enable acceptance) they can do it in literally any other country.

In short, these organizations are being forced to move along the learning curve in a way that would have never happened if Bukele hadn’t forced the issue. If they want to continue trading within the borders, they will have to find a process that works. Once they have it, it seems quite likely that some of them will simply duplicate it in other territories.

Some may even proactively use it as a positive public relations spin, directly appealing to the millions of millennials who are both their target audience and most likely to engage with it. It’s a win-win.

Boosting Bitcoin use

Anybody who is the first to do something merely breaks down the perceived barriers of doing so. It shows that it has always been possible, if only you had the will to do it in the first place.

When Roger Bannister broke the four-minute mile barrier in 1954, he was followed by countless others who now knew — for certain — that it could be done. Over time, this belief led to improved times and the current record is 3:43:13, set in 1999 by Hicham El Guerrouj, nearly 16 seconds faster than Bannister’s original finish.

Bitcoin adoption will see the same incremental improvements as other countries follow the same path. It seems certain that other Latin American countries will be first in line with Paraguay, Panama, Brazil, Mexico, and Argentina making positive noises about doing so, but other countries, such as Tanzania as a topical example, have also started to pave the way for a possible Bitcoin adoption of some sort.

It’s likely that they may adopt a “wait and see” approach as the law is implemented, learning from the hiccups and unforeseen issues that will almost certainly occur. El Salvador may find itself in a position to provide consultancy services to other sovereign states, either directly or through the commercial layer.

A precedent for a precedent

But even El Salvador has a proven case study to look at.

During his speech, Mallers revealed some incredible numbers. According to his data, around 22% of the total GDP of El Salvador is made up of remittances. In other words, 22% of the capital influx of the country is sent from abroad. Since its GDP was last reported as being $24.61 billion in 2020, we can conclude that this figure is around $5.4 billion.

Most of this comes from the 2,311,574 (Source: 2019 US Consensus) El Salvadorians who live and work in the U.S., and since their native country currently only has a population of 6,517,678 according to Worldmeters.info, that means that 26% of all nationals live abroad.

Yet the most shocking number is the remittance fees: according to both Mallers and Bukele, up to 50% of the total sent to the country from the U.S. is lost to fees. On that (worst case) basis, somewhere around another $5.4 billion is transferred from some of the poorest people on the planet to the banking system in the U.S. Every. Single. Year.

Bitcoin, as the old adage goes, fixes this.

Using Bitcoin, fees drop instantly to a fraction of this and, theoretically, it means the country can expect to increase its GDP overnight by 22% assuming the remittances remain at the same value. That money is simply redirected from the international banking system directly to the pockets of the citizens of El Salvador.

And we know this because we have already seen it. According to a speech given recently by Ray Youssef, CEO of the peer-to-peer trading platform Paxful, remittances sent to Nigeria via traditional routes dropped from $2.5 billion to just $55 million between January 2020 and September 2020. That’s a drop of 98.7%, coinciding with the same increase in bitcoin-based remittances.

On the same cost basis, that’s another $2.45 billion moving out of the banking system directly into the pockets of the poorest people on the planet. And remember, this is to a country that is currently intent on making life as difficult as possible for any citizens who want to use Bitcoin. How different will it be in a country where it is not only legal, but actively encouraged?

So, tell me again, how exactly does Bitcoin have no use case?

Bitcoin and the threat of oppression

Interestingly, reaction to the news by mainstream media was mixed. I was personally contacted by dozens of journalists seeking comment on what I thought about Bitcoin being adopted by an “authoritarian” regime. Use of the cryptocurrency is, after all, touted as a “tool of freedom” and there was some debate about just how “free” El Salvador actually is.

Bukele’s removal of certain high-profile lawmakers, something he did fairly early on in his presidency, is an excellent example. For his supporters, it was a necessary move to wipe out corruption. For his detractors, it was a frightening display of almost totalitarian control.

Like most things, the truth is probably somewhere in the middle, and asking someone from El Salvador will render you an answer depending on the lens they view it through.

In short, it’s a classic case of “one man’s freedom fighter is another man’s terrorist.”

The country also suffers from a very high (although broadly falling) crime rate, inequality and even some suggestions of human rights abuse. One anonymous Redditor posted a “warts and all” thread about El Salvador that went fully viral as the news was digested. Many agreed with the post.

Many didn’t.

However, this is all a distraction if we take the time to zoom out and look at this objectively. We don’t actually need to understand where Bukele is on the scale of dictators — or even if he registers at all — to understand how universally good this could be for the country under any scenario.

Bitcoin does not care what kind of economy you run. Your government is irrelevant, as are your officials and richest organizations. Sure, they are free to use it, but Bitcoin is bigger than you. It’s bigger than any of us. Heck, it’s bigger than all of us.

By encouraging its use, you are giving your citizens a degree of financial freedom that even many fully developed western countries cannot currently offer.

That, in my mind, does not fit with something an oppressive dictator would do. However, I also concede that I am not qualified to comment, since I live many thousands of miles away.

So, we’re left with the idea that either Bukele has an excellent understanding of Bitcoin and has just given his citizens permission to engage openly in a future-proof payment system that is almost certainly irreversible once started, or he is a dictator with a woeful understanding who has made a terrible mistake if he thinks he is now going to be able to control the financial activities of his people.

Applying Occam’s Razor, it seems most likely this was done for the reasons we’d all like to believe it was done — that is, for the overall good of the people, country and economy.

The final word

El Salvador is just the first. Others will follow and they will learn from the implementation errors that will inevitably be made as they always are when something is done for the first time. Next time it will happen more quickly and more easily.

It is also a perfect case study, a small, self-contained example of just a few million people. At the same time, it is an entire state-level ecosystem, neatly packaged for the implementation of a turnkey solution.

In some ways, many of us would be tempted to consider El Salvador a little backwards when compared to our advanced, tech-driven, abundant and relatively crime-free societies. Yet, Bitcoin use for daily transactions, especially via the Lightning Network, is common place. Many of their citizens know how to use it, account for it and secure it better than you or me.

Make no mistake, they are true pioneers, and in every sense of the word.

And if we’re not careful, we might find one day that we’ll be playing catch-up to the El Salvadorians.

Special thanks to Diego Dominguez, resident of El Salvador, for double checking some of the local aspects of this article.

Want articles and to minute analysis and opinion in your inbox? Why not subscribe to the ‘Bitcoin and Global Finance’ newsletter? Receive special offers and insider info. Unsubscribe at any time.

Disclosure: The author of this opinion piece has been heavily involved with bitcoin for several years and holds a substantial cryptocurrency portfolio, including bitcoin. He also has a mining operation running the SHA-256 algorithm based in Siberia and is a published author on the subject of promoting the understanding of cryptocurrency. Jason is an analyst at Quantum Economics and consultant to Luno.

Disclaimer: Investing in any asset class is risky. The above should not be taken as financial advice, nor construed as so. Always do your own research before investing or consult with a professional financial planner.

Fortune favors the bold and I truly believe that EL Salvador will be recognized by history as being the first society to truly embrace the digital paradigm shift.

I believe the world bank is a consortium of countries that will eventually capitulate to Bitcoin, but not after fighting to have it removed from the face of the Earth.

Too bad they will lose.

Nice Article Jason

"World Bank rejects El Salvador's request to help implement bitcoin as legal tender"

This was the Latest news about Bitcoin today and this news broke many hearts that why can't the world understand Bitcoin after so many years has passed on

I just wanna say that Changes occur slowly one Bad news shouldn't change the Chart of Our BTC

We should believe in Bitcoin more then this news and If it's 1000% true just wait the right time will come and we will see Bitcoin Accepted by Whole World

The day will come soon we just have to wait and believe

Jason if you can give a brief about this headline in your new article that would be awesome

Sorry if i did a mistake writing any words guys :D

Hope you all also agree with my words :)